START HERE - INDUSTRIAL PROPERTY GUIDES

1Industrial Property Rental - Practical Guide

2Industrial Property Rental By Location

3Warehouse & Factory Rental Rates - Real Market Guide

Explore Popular Locations

Featured Listings

Recently Sold Properties

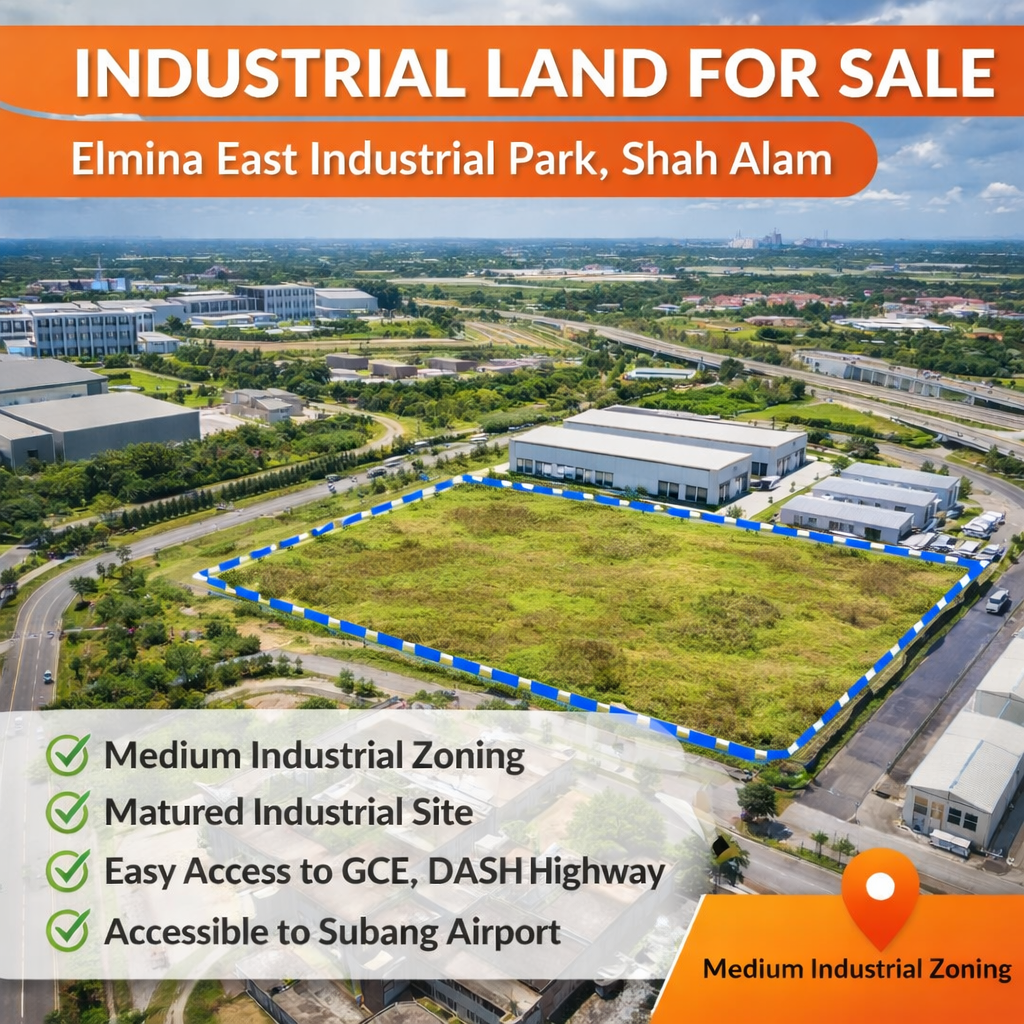

Selected industrial property transactions for market reference and price benchmarking.

Elmina East Industrial Park , Shah Alam

Transacted Price

RM 11,197,510

Transacted Date

Feb 2025

Land Area

56,553 sqft

Meru , Klang

Transacted Price

RM 8,450,000

Transacted Date

Feb 2025

Land Area

24,918 sqft

Elmina Business Park , Sungai Buloh

Transacted Price

RM 5,500,000

Transacted Date

Jul 2025

Land Area

11,323.73 sqft

Bandar Bukit Raja , Klang

Transacted Price

RM 4,100,000

Transacted Date

Mar 2025

Land Area

7,922 sqft

Not Sure What Your Property Is Worth?

Latest Properties

Klang

RM 56,000

See More Properties In

BEHIND THE NAME

Vincent Yim

Industrial Property Advisor, E1283

Industrial property decisions are rarely simple.

Warehouse, factories and inductrial land involves more than just price - how a site works day to day matters.

I advise owners, operators and investors on industrial properties across Klang Valley, with a focus on practical fit and long-term suitability.

I also assist selected commercial and residential clients where location and broader planning are involved.